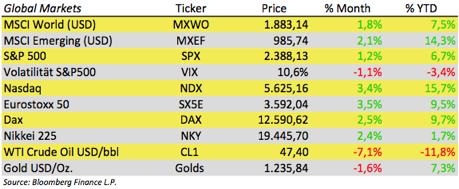

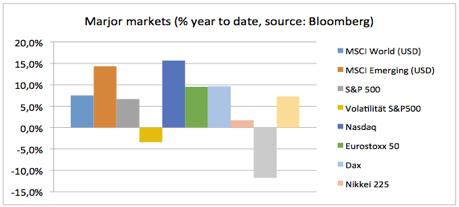

Equity markets have gained as much as 5% versus ournewsletter two weeks ago, interest rates are nearly unchanged while gold andcrude oil went down.

The biggest gain has come from Europe this time -celebrating the results of the first round of French presidential elections.Centrist Emmanuel Macron and far-right leader Marine Le Pen will go head tohead in the French presidential runoff on May 7. Recent surveys see Macronwinning the runoff by more than 60 percent. Although the result is a massiverejection of the ruling establishment, it is a pro-EU vote sparking a reliefrally led by EU stocks, and in particular by the banking sector.

The EU economy presents itself increasingly in good shape. ECB president has characterized the euro-area recovery “solid and broad”. Unemployment is steadily declining from a peak of more than 12 percent in 2013, with improvements also visible in crisis-hit countries such as Spain. See also our chart of the day!

Better chances of finding a job make consumers more willing to spend. Euro-area economic confidence hit its highest in a decade in April, and an index of consumer sentiment is close to its strongest reading since before the financial crisis.

Stricter budget constraints in many member countries have caused the eurozone’s combined public deficit drop to levels last seen in 2008. The dip was caused mainly by decreasing government spending, Eurostat reported. The level of government borrowing across the 19-member eurozone has fallen to 1.4 percent which is the lowest level since the global financial crisis. While core inflation shows the strongest in almost four years, the ECB cautioned that price growth still lacks a convincing upward trend.

By contrast the US Fed is one step ahead signaling the next interest rate hike for June 2017. Currently the Fed funds futures indicate a 97 percent chance of a June interest-rate hike. Accordingly investors take this step for sure after latest comments by Fed officials.